About Kam Financial & Realty, Inc.

Table of Contents5 Easy Facts About Kam Financial & Realty, Inc. ShownThe 6-Second Trick For Kam Financial & Realty, Inc.Indicators on Kam Financial & Realty, Inc. You Need To KnowWhat Does Kam Financial & Realty, Inc. Do?Little Known Questions About Kam Financial & Realty, Inc..Fascination About Kam Financial & Realty, Inc.

When one takes into consideration that home loan brokers are not called for to file SARs, the actual quantity of home mortgage fraud activity can be a lot higher. https://www.pageorama.com/?p=kamfnnclr1ty. Since early March 2007, the Federal Bureau of Investigation (FBI) had 1,036 pending home mortgage scams investigations,4 contrasted with 818 and 721, respectively, in the 2 previous yearsThe bulk of home loan scams falls under two wide groups based on the inspiration behind the fraud. generally entails a borrower who will certainly overemphasize earnings or asset values on his/her financial declaration to get approved for a loan to buy a home (mortgage broker in california). In a lot of these situations, assumptions are that if the income does not increase to fulfill the payment, the home will be cost a profit from recognition

Getting My Kam Financial & Realty, Inc. To Work

The vast bulk of fraudulence instances are found and reported by the establishments themselves. Broker-facilitated fraudulence can be fraud for building, scams for earnings, or a mix of both.

The following represents a situation of fraudulence for earnings. A $165 million community bank determined to enter the mortgage banking service. The financial institution purchased a small home loan business and worked with a skilled home loan banker to run the operation. Almost 5 years right into the relationship, an investor alerted the bank that several loansall stemmed via the very same third-party brokerwere being returned for repurchase.

Our Kam Financial & Realty, Inc. PDFs

The financial institution notified its main federal regulatory authority, which then called the FDIC due to the possible influence on the financial institution's economic problem (https://telegra.ph/Your-Trusted-Mortgage-Loan-Officer-California---KAM-Financial--Realty-Inc-08-28). Additional investigation revealed that the broker was operating in collusion with a building contractor and an appraiser to flip properties over and over once more for higher, invalid revenues. In total amount, greater than 100 financings were originated to one building contractor in the very same subdivision

The broker rejected to make the payments, and the situation entered into litigation. The financial institution was eventually granted $3.5 million. In a succeeding discussion with FDIC supervisors, the financial institution's president showed that he had actually always listened to that one of the most challenging component of mortgage financial was ensuring you implemented the best bush to counter any passion rate run the risk of the financial institution might sustain while warehousing a substantial volume of home loan finances.

Get This Report about Kam Financial & Realty, Inc.

The bank had depiction and service warranty clauses in contracts with its brokers and thought it had recourse relative to the financings being originated and marketed with the pipeline. During the lawsuits, the third-party broker said that the financial institution needs to share some responsibility for this direct exposure because its inner control systems need to have acknowledged a lending concentration to this neighborhood and instituted steps to prevent this risk.

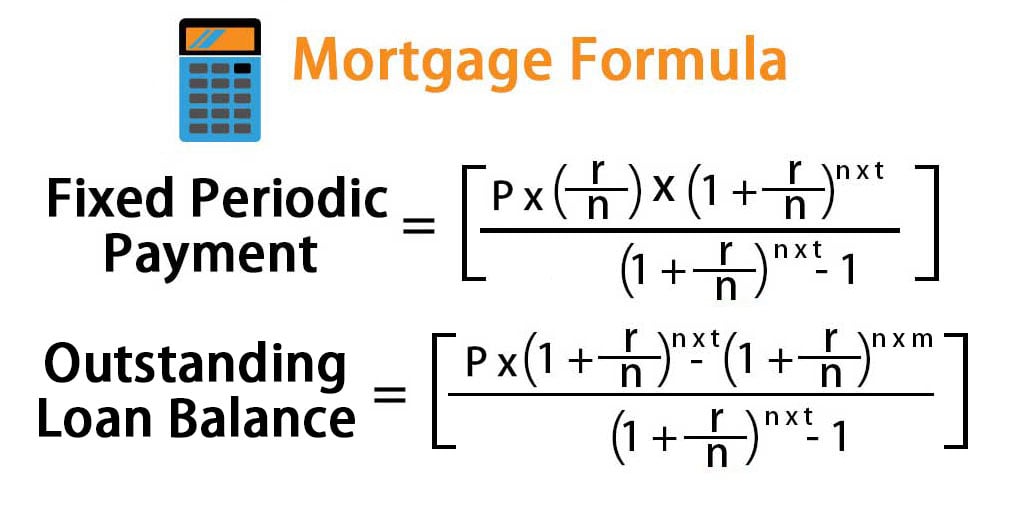

What we call a regular monthly home mortgage payment isn't simply paying off your mortgage. Rather, think of a regular monthly home mortgage repayment as the 4 horsemen: Principal, Passion, Home Tax, and Homeowner's Insurance policy (called PITIlike pity, because, you know, it boosts your repayment).

Hang onif you believe principal is the only quantity to consider, you 'd be failing to remember about principal's finest close friend: rate of interest. It would certainly be wonderful to think lending institutions allow you borrow their money just due to the fact that they like you. While that may be real, they're still running a company and intend to put food on the table also.

The 10-Minute Rule for Kam Financial & Realty, Inc.

Interest is a percent of the principalthe quantity of the loan you have entrusted to repay. Interest is a percentage of the principalthe quantity of the loan you have actually left to settle. Home mortgage rate of interest are frequently altering, which is why it's wise to select a home mortgage with a fixed rate of interest so you know just how much you'll pay every month.

That would suggest you 'd pay a monstrous $533 on your very first month's mortgage settlement. Obtain all set for a little bit of pop over to this web-site mathematics right here.

Excitement About Kam Financial & Realty, Inc.

That would certainly make your month-to-month mortgage repayment $1,184 every month. Month-to-month Principal $1,184 $533 $651 The following month, you'll pay the same $1,184, but less will most likely to passion ($531) and more will go to your principal ($653). That pattern continues over the life of your home mortgage till, by the end of your mortgage, virtually all of your settlement approaches principal.